Blockchain: A Brief Summary

Generally speaking, blockchain technology is a peer-to-peer computer network that uses cryptocurrency to record transactions and track assets, both physical and intangible. These transactions can be recorded, copied, and stored on each server, or “node,” and are referred to as blocks. This is linked to the network.

Blockchain is essentially a decentralized database that is managed by various individuals, unlike traditional databases that store records in a centralized particular place.

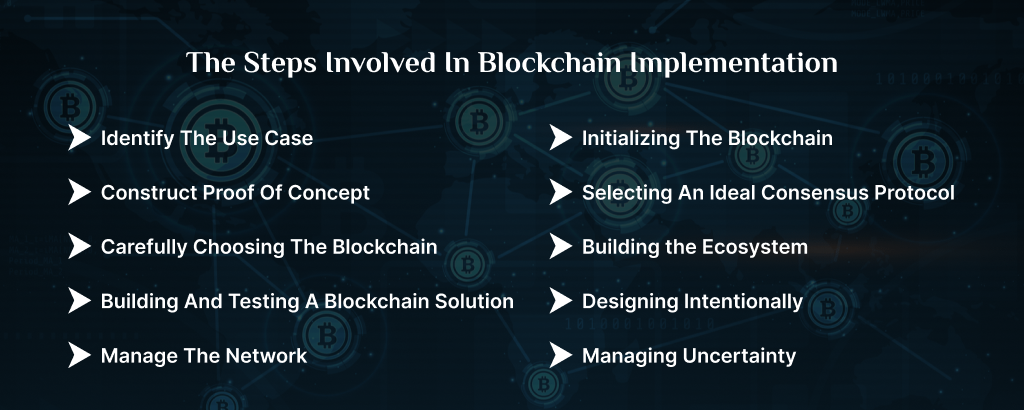

The Steps Involved In Blockchain Implementation:

Everyone who works with digital currency should be acquainted with the blockchain industry. We have done a lot of studies and believe that blockchain technologies have the potential to completely change your company. Use these ideas for blockchain implementation.

- Identify The Use Case:

This is the crucial first step in the implementation of a blockchain, to begin with. In order to identify the use cases, you must first evaluate, define, and organize your blockchain requirements. Implementing blockchain solutions ensures that they will aid in resolving the exact issues you desire to solve.

You need need to ask yourself a few questions after identifying your use case, such as:

-

- Why exactly is a blockchain essential for my business?

-

- Is blockchain technology the ideal solution for my company’s issue?

-

- Why is it necessary for our company to use blockchain technology?

-

- What are my goals, targets, and objectives if I choose to implement a blockchain?

These related questions could make it clearer to you why you require blockchain implementation in our company.

- Construct Proof Of Concept:

Constructing a proof of concept occurs after you’ve identified the many possibilities for your use case. The term POC simply refers to a strategic process used to assess how practical a blockchain implementation is for your company.

Proof of concept evaluates the project’s functionality and viability as a means of completing a goal. Creating a competent POC will ensure automation, streamlining intermediary and repetitive actions. The blockchain Proof of Concept provides end users and consumers with far larger value than competing solutions.

Today, a wide range of sectors use blockchain in their everyday work and rely on PoCs for maximum effectiveness.

-

- Telecom

-

- Management

-

- Fintech

-

- KYC

-

- Insurance, among others.

- Carefully Choosing The Blockchain:

When choosing the best blockchain platform for your company, you must be very careful. When companies and organizations are given the choice to use blockchain, they develop a false belief. This is a strategic action that will assist you in taking into account variables like your budget and careful study. It is crucial that they give blockchain significant thought before deciding it isn’t the ideal solution.

Blockchain improves value for businesses even though it isn’t a universal technology. The following are a number of the top blockchain platforms:

-

- Quorum

-

- Ethereum

-

- Stellar

-

- Solana

- Building And Testing A Blockchain Solution:

If you are a new user, you should first identify yourself with the blockchain technology in use today. Therefore, you can choose and use the blockchain that enables you to customize it to suit your needs. Before deciding on blockchain technology, you need to consider a number of factors, such as:

-

- Technology depth refers to the security, consensus, and support for both public and private blockchains.

-

- Technology breadth entails support for numerous platforms and multichain.

Smart contracts are the central component of blockchain technology. This enables individuals to transmit crucial goods without the need for a central third party. The contracts can have the rules you need to be attached to them.

-

- Manage The Network:

To manage the entire network on the production of a particular chain, first, create your own block. The power required to ensure the persistence of the communication nodes is engaged using the encrypted token.

- Initializing The Blockchain:

The first block must be manually picked in need for the blockchain to be Initializing. Keep in mind that the block should include every element of the specified chain. The features are then distributed among network nodes.

It is suggested that you begin hybrid solutions that are both on-chain and off-chain objects, on the cloud server.

- Selecting An Ideal Consensus Protocol:

-

- Proof of Work:

This protocol rewards miners for resolving challenging equations. They support your efforts to secure against cyberattacks and verify transactions to create new blocks.

-

- Proof of Stake:

This is another consensus protocol in which the developer of the next block will be chosen based on a variety of random qualities that may include age, money, performance, etc.

-

- Delegated Proof of Stake:

The stakeholder election of the miner who would create the following block makes this more democratic.

-

- Byzantine Fault Tolerance (BFT):

This protocol describes a situation in which several network components might fail. even when a few nodes only sometimes send out misleading information.

-

- Proof of Weight:

In Proof of Weight, an agreement is achieved based on the weight and amount of cryptocurrency that the miner owns.

- Building the Ecosystem:

An ecosystem is required once a large number of parties start interacting with the blockchain. A network within the wider blockchain community will be the ecosystem.

It will serve to promote business trust and help in the improvement of understanding of the blockchain industry. The following challenges must be resolved by the stakeholders before an ecosystem can be built:

-

- The contract’s terms.

-

- How to ensure that costs and benefits are distributed equitably.

-

- the establishment of governance structures.

- Designing Intentionally:

Every blockchain expert would agree that careful design is needed for the blockchain’s structure. The design must be thoughtfully executed to ensure that any organizational problems are quickly resolved.

- Managing Uncertainty:

Blockchain regulations’ future is still mostly uncertain. It is crucial to continue with the review of these rules and to actively participate in the development of these policies because of this.

You should try to encourage the decision-makers in your country to support expanding the use of the blockchain industry because these policies differ from one nation to the next.

More Information About The Company:

Numerous modifications are necessary for the implementation of blockchain, and this simplified your work considerably. You must make sure that your user interface is easy to use and reasonably priced for your customers. Despite any difficulties with blockchain implementation, the information in this article will tremendously assist you in achieving your goals in the blockchain industry.

If you want to implement blockchain technology in your business, the first thing you need to do is look for the best blockchain development company that can assist you in creating amazing blockchain technology. One of the top blockchain technology companies with a skilled development staff is Rain Infotech Private Limited. That might facilitate faster business growth for you.